Foundation of a Sound Financial Plan

The purpose of insurance is to manage and mitigate your exposure to risk. We often refer to ourselves as financial architects. Just as you would have a blueprint for building a home, we believe it is vital to have a financial blueprint. Your financial house is made up of many rooms. We work to help you determine how much you need, financially in each room, understand when you need it, then discuss, develop and implement the best strategies to get there. The most important and least appreciated part of any home is its foundation. Here we focus on the analysis of needs in the event of death or disability. If the foundation is not the proper size and quality, then everything we strive to build could collapse when a death or disability strikes.

-

Disability Income Insurance

Disability income insurance protects you in the event you become mentally or physically unable to work. If you were to be injured in an accident, or diagnosed with a serious illness, it may be difficult or even impossible to continue earning a living and supporting your lifestyle.

In these instances, individual disability income insurance is designed to replace a certain amount of your income. Even though you may have group long-term disability insurance through your employer, it may not be enough.

-

Life Insurance

Life Insurance can be broken down into two types.

Term: An affordable solution to addressing an unexpected death during a limited number of years.

Permanent: Provides coverage for life with a death benefit that can grow over time and accumulate cash value that you’ll have access to throughout your lifetime.

Your health, your family’s financial needs today as well as in the future are important considerations when determining the right amount and type of life insurance coverage.

-

Business Insurance

The monthly business expenses of your practice don’t stop when an injury or illness prevents you from working.

Business overhead expense insurance can be used to help pay those bills until you’re able to return your practice.

Buy/Sell Insurance Funding: Protects your investment, the investment of your partners and the value of your practice. A buy/sell insurance policy can prepare your practice with a predetermined valuation method for each partner’s share and an agreed upon plan for continuity.

-

Long Term Care

Should a serious illness, accident, or injury cause you to need assistance with your daily activities, or should you have a severe cognitive impairment, Long Term Care insurance can provide the funding that allows you or your family member to receive the care they want — in the setting they choose. It can also help protect assets, retirement funds, and an estate from being depleted to provide care.

The time to create a plan is now, while you are healthy. The earlier you begin planning, the more options you may have to continue living life on your terms.

Disability Income Insurance

Disability income insurance protects you in the event you become mentally or physically unable to work. If you were to be injured in an accident, or diagnosed with a serious illness, it may be difficult or even impossible to continue earning a living and supporting your lifestyle. In these instances, disability income insurance is designed to replace a certain amount of your income. Even though you may have group long-term disability insurance through your employer, it may not be enough.

Disability income insurance payments can help you continue covering your living expenses and financial obligations, so you may be able to keep your home, pay your bills, and avoid spending down your retirement savings, and racking up credit card debt.

Why is Disability Income Insurance Especially Important for Physicians?

Many physicians have dedicated close to a decade to training and invested over $200K in their education. When a medical professional loses the ability to practice in his or her specialty, it’s almost impossible to find a replacement career with a comparable salary.

When Should I Get Disability Income Insurance?

The younger and healthier you are, typically the lower rates will be and the easier it is to get approved. Often, many medical schools and residency programs offer discount programs with streamlined underwriting for young physicians. During last year of med school and residency training are great times to secure disability insurance, because it is likely your rates will never be lower. However, make sure to get a policy with the future insurance rider* that allows you to increase coverage as earnings rise in later years.

*Riders are available at an additional cost and subject to state availability.

4 Key Components to Consider… When Buying Disability Insurance

-

TRUE OWN OCCUPATION disability insurance protects you in disability insurance protects you in the event you’re not able to do the duties of your own occupation. You can receive coverage even though you may be able to work in another area of medicine or a different career altogether. Under this definition, if you’re not able to do the duties of your primary occupation, you will be eligible to receive a paycheck from the insurance company. You can receive benefits even if you’re earning an income from working in another specialty or profession.

Non-cancelable & guaranteed renewable: This states that the insurer cannot raise your premiums nor cancel your policy or change the terms and features of your contract as long as you continue paying your premiums.

Future Increase Option: This provides the opportunity to increase coverage annually without having to provide evidence of good health. It’s your choice whether or not to apply for additional insurance coverage in any given year.

Partial Disability: Protects you by paying a partial benefit if you suffer an injury or illness that limits your ability to perform certain types of care or procedures but doesn’t cause total disability.

Cost of Living Adjustment: A rider that states the insurance company will increase your benefit to account for inflation.

Catastrophic: Provides extra income replacement funds– if you are functionally impaired or irrevocably disabled.

-

How to apply for disability insurance and what it costs:

When you choose to purchase a personal policy to protect your future you’re not tied to a particular practice or employer, because individual coverage stays with you as long as you pay your premiums. As these plans are almost always paid for with after-tax dollars, the benefit income they provide is usually tax-free.

A popular rule of thumb is to expect to pay between 2% to 4% of your annual salary for this type of coverage. Much of that variation is depends on the terms and provisions you choose for your policy, including:

Medical School & Hospital Discount programs: often discounted disability programs are offered to students just prior to graduating medical school as well as during residency training. These discounts can be a permanent part of your policy and may apply to future additions of coverage. Be sure to ask us about the discount programs we offer to academic institutions and hospitals throughout the country.

The benefit amount: The more you receive for each month of disability, the higher the cost of the policy.

The waiting period: If you have enough savings or assets to tide you over, you can lower premiums by choosing a longer waiting period.

The benefit period: The shorter the benefit period, the lower the premiums.

The definition of disability: While not recommended for physicians, if you forego an own-occupation definition, your premiums will be lower.

Optional riders: While some riders may be included at no extra charge, others will add an incremental cost to your plan.

No matter what terms and provisions you choose, much of your actual policy cost will be determined on by the statistical risk you present to the insurance company. That risk will be analyzed and calculated during an underwriting process that takes into account a number of factors, including:

Medical specialty: Higher risk specialties are those that perform interventional procedures, such as surgeons, and emergency room doctors; by contrast, GPs tend to be classified as lower risk.

Age: To obtain the best rates, don’t put off getting insurance coverage, particularly while you are healthy.

Health: Expect to answer questions about your family medical history, pre-existing conditions, tobacco, and alcohol usage.

Finances: Since benefit amounts are calculated as a percentage of your earnings, the insurer will evaluate all your sources of earned and unearned income.

Location: As a rule, insurance regulations, living costs, and income vary by state; these are reflected in your policy costs.

-

The terms of your disability income insurance contract should be strong and align with what is needed to protect your income. The cost of the contract needs to be affordable. But it also recommended you review the financial strength of the company you choose to protect you throughout your career. Independent financial ratings are considered to lead indicators of a company’s ability to pay claims 10, 20, or 30+ years into the future. Take the time to research the carriers before choosing who will be insuring your greatest asset.

-

Contract, Cost, and Company are no doubt vital components in the disability income insurance decision-making process. But it is at often at claim time when our clients most appreciate the value of our relationship. Receiving devastating diagnoses or being involved in a debilitating accident are extremely trying times in people’s lives. We know that applying for disability benefits can be daunting, especially for those who bought coverage online without the dedicated care of a trusted advisor. We believe being there for our clients at the time of claim is one of the most critical times in our relationship. We make it a priority to connect with our clients and/or their family members assisting them during this process, and allowing them more time to focus on treatment and recovery.

Life Insurance

Term Life Insurance

Term life insurance was created as an affordable solution to addressing an unexpected death during a limited number of years. For a fixed number of years, term life insurance can provide your dependents or lenders with a substantial safety net. This makes it a common choice for physicians who want to ensure their loved ones are financially secure in the event of their untimely death.

While the need for term life insurance varies, it’s frequently used to protect family, provide an estate in the event of premature death, and serve as collateral for business and other loans.

Important Term Life Insurance Options

Common considerations when purchasing these policies are the number of years you expect to earn an income and the amount your family needs to sustain their lifestyle without you (mortgage, tuition, car payments, monthly bills).

At a Glance: Term Life Insurance

Compared to some other options, term life insurance is often used to provide a large benefit to young families for relatively low premiums.

Common coverage terms are between 10 and 30 years.

Benefit amounts are typically static.

Policy premiums can be level or begin at a lower rate and increase annually.

Term life may be combined with permanent life to meet coverage needs.

Once the set term has been reached, some policies can be renewed at increased cost, terminated or converted into a permanent life policy (you may be required to go through additional underwriting).

Common uses include:

Providing living expenses for dependents

Paying off mortgages and loans

Small business loan collateral

Funding buyout agreements between partners

Permanent Life Insurance

Long-Term Protection & Growth for Your Future

Permanent life insurance can provide a death benefit for your family that may grow over time.

Permanent life policies are long-term coverages that may grow in value. Many of these policies also allow you to access or borrow against a portion of the benefits, called the policy’s “cash value.”

Permanent Life Insurance at a Glance

Includes whole life, universal life, and variable universal insurance options

Created for long term life insurance needs

Policies may accumulate cash value that may be withdrawn or borrowed upon

Premiums can remain level, increase, decrease, or discontinue

Commonly used for legacy planning to provide for family as an inheritance

Business Overhead Expense Insurance

Your Practice’s Everyday Expenses

The monthly business expenses of your practice don’t stop when an injury or illness prevents you from working. Business overhead expense insurance can be used to pay those bills until you’re able to return your practice.

A Financial Lifeline for Your Practice

Protect your fiscal health by continuing to make payments on loans related to your practice, even when a disability curtails your ability to earn an income. Explore the benefits of business loan protection insurance and options available to you, with the help of our team.

While disability income insurance can supplement your personal income in the event of an accident or illness, it doesn’t cover ongoing practice expenses. Business overhead expense insurance is designed to cover those fixed business expenses that can’t wait until you recover or sell the business, including staff salaries, taxes, utilities, office leases and more.

Covered expenses may include:

Staff salaries

Utilities

Some business insurance premiums

Professional dues

Property taxes

Accounting and legal fees

Rent

Interest payment on business premises or equipment

Principal or depreciation of business premises or equipment

Disability Buy/Sell Insurance

Preparing Your Practice for the Unexpected

Disability income insurance can provide for you when an injury or illness hinders your ability to work. It does not help you when one of your partners in the practice is disabled long term and you are faced with having to purchase their shares. For those situations, disability buy/sell insurance may help provide the funds to purchase the disabled partners share of the practice helping to ensure continuation of the practice.

Protecting You, Your Partners, and Your Practice

Protect your investment, the investments of your partners and the value of your business. A buy/sell insurance policy can prepare your practice for the unexpected, with predetermined valuation method(s) for each partner’s share and an agreed upon plan for business continuity.

Disability Buy/Sell Insurance at a Glance:

In the event of a partner’s disability, a buy/sell insurance policy can pay the disabled partner for their share of the practice, dissolving their interests in the business.

Since the market value of a practice can be affected by the disability of a partner, buy/sell agreements can set a predetermined valuation method of each partner’s shares.

Many plans include a waiting period, known as an elimination period before disability benefits are paid. This time is set aside for potential recovery from the disabling injury or illness.

Plan payouts may be a lump sum or paid over a predetermined period of time.

Benefits are paid in accordance with an underlying buy/sell agreement.

Long Term Care

The need for long term care may happen to anyone… at any time. It could be you, your spouse or partner, a parent, or even a sibling. The need for long term care may result from being chronically ill, from a severe cognitive impairment or something as unexpected as an accident or injury.

The time to create a plan is now, while you are healthy. The earlier you begin planning, the more options you may have to continue living life on your terms.

Should a serious illness, accident, or injury cause you to need assistance with your daily activities, or should you have a severe cognitive impairment, a plan can help you prepare to receive the care you want — in the setting you choose. It can also help protect your assets, retirement funds, and your estate from being depleted to provide care.

The plans you make today could impact your future lifestyle, and the quality of life you experience.

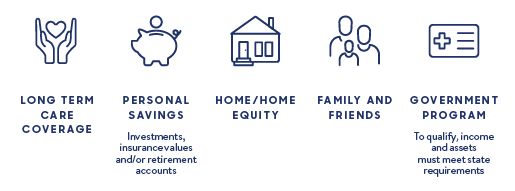

What is long term care?

Long term care is a variety of services and supports to help meet personal care needs over an extended period of time. Long term care may involve non-skilled personal care assistance, such as help performing everyday Activities of Daily Living (ADLs), which are: bathing, dressing, using the toilet, transferring (to or from bed or chair), caring for incontinence and eating. Long term care services may help you maximize your independence and functioning at a time when you are unable to be fully independent.

Will a need for long-term care impact the entire family?

A need for long-term care may have a substantial impact on your relationships with family or friends. Sacrifices may be made to provide for your care. Family or friends may have to give up free time, spend less time with their family, and take on the stress and physical strain of becoming your caregiver.